So, the operation of Credit Cards is apparently stuck in the last Century. The major suppliers of credit cards have not kept up with the requirements of the modern age of online transactions.

On-line Credit Card Fraud is a Major Headache

Case in point: My credit card was used Fraudulently. I have a couple of cards, one for physical transactions where I’m always present – well almost always present. And another that I only use On-Line. Of course, the fraud involved the credit card that was used online. I purchased some Game Currency from a game I play a lot for $10, and less than a week later someone tried to purchase $5599 at Best Buy. There was a lot of confusion about whether the transaction occurred On-Line, but the address was given as Minneapolis, Minnesota. Which is far from where I live. So the transaction was declined, and I was alerted. But that’s not the end of the problem. That card number is now stopped. It can no longer be used. And if this were last century, I could just use another of my few cards to eat take-out at restaurants, or buy groceries.

But this is 2020, and that credit card is in the hands of over a dozen on-line merchants whose computers will automatically try to use it on some random schedule to provide services that I use. These include Netflix, my internet service, my satellite tv service and so forth. I’m “waiting four to five business days” for the new card to arrive. And any of these days one of these many services’ computers might try to use that dead card. To say nothing of the fact that it will take an hour or so to go through all the services’ websites and give them a new card number. I need a better way.

Virtual Credit Card Numbers

A virtual credit card number, or a Digital Card or a Controlled Payment card is a better way. Even Wikipedia can’t write one article on the subject.

Bank of America Tried VCCs

A few years ago, Bank of America had a service with their credit cards that allowed creating “Virtual CC Numbers”. You could set the spending limit and the expiration date and when the card was first used, it became “Merchant Locked” which means that using the card for any other merchant would automatically fail. I forget what the service was called. It was odd in that it used a “Adobe Flash” app that launched in the browser from the BofA website to create or manage these card numbers. Clearly they thought cute animations were more important than security since flash is a well known attack surface. So much so that it will be phased out completely soon. And BofA no longer provides this VCC service. Just dropped it completely.

Capital One has VCCs, But not Enthusiastically

A couple of years ago, Capital One created ENO. How clever of them to spell ONE backward.

A couple of years ago, after a previous instance of Fraud on a credit card – the 3rd in a year – I signed up with Capital One to use ENO, but then found that I could not because my Tracfone mobile phone carrier was not a supported phone carrier. Only the “Major Phone Carriers” were supported at the time.

What I find now is that the folks you talk to on the phone about your credit card fraud do not know about ENO, cannot answer your questions and do not enthusiastically encourage you to sign up and use ENO. Instead they talk about verifying that you are you so that they can “Mail you a new card in four or five days” and mention that they have “Stopped all further transactions on the card you have.” How helpful.

How to Get a VCC Service?

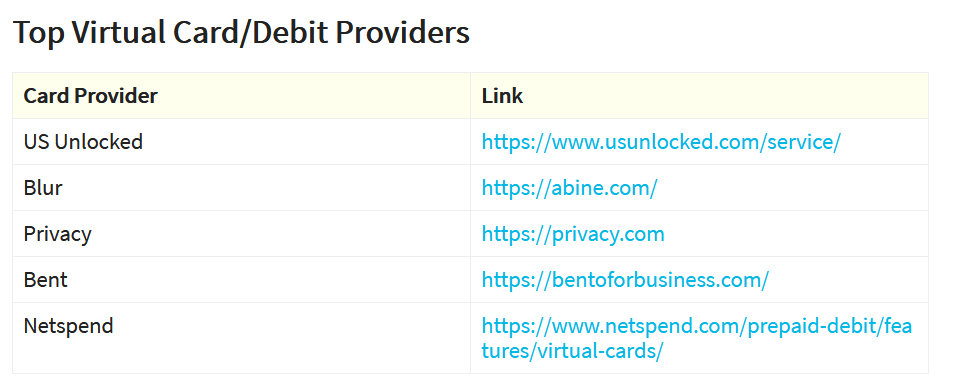

I’m not clear why Credit Card companies are not wildly enthusiastic about supporting Virtual Credit Card numbers, but they aren’t. They are leaving this opportunity wide open for Privacy.com and some other companies.

The web site is here for this list.

But the Problem Is…

The problem is that these virtual credit card companies [VCCC] do not provide the same guarantees that credit cards provide. The major one of these being that if I dispute a charge, the assumption is that I did not charge it. Rather than having to prove that I did not charge it. This was carefully written into the law governing credit cards. And it does not hold for Debit Cards.

These VCCC require a Debit Card, or a Bank Account Number to “Fund” the virtual credit cards that you use. I have been unwilling to give these companies my only checking account for them to make a mistake with.

And the Solution May Be…

But there may be a solution to this problem.

How about I have a second checking account; at the same bank where I bank, and managed online with my other account. But with only some money there so if there’s a problem, all my funds are not at risk? Sure, the bank says. No problem. No monthly fees either. And they signed me up in an hour over the phone with an email signature.

The only problem is…

But here’s a glitch. At Privacy.com [ This is not an endorsement of Privacy.com. I have not used them yet, and am not compensated by them in any way.] I could not “Fund” my Privacy.com account using my bank. It tried to work, apparently through a service called Plaid.

But my bank didn’t accept the transaction, even though my bank robot called me with a one time code. So it looks like I need a “Debit Card Number” for my new checking account to sign up with Privacy.com. I’ll see if the bank can get me a Debit Card number quickly on a Sunday. They made me a checking account over the phone on a Saturday. But I made the mistake of asking not to have a Debit Card.

We’ll see. I’m hopeful that this will work. Finally control over my online purchases.

Privacy.com provides a free and a paid service. I’ll probably need the paid service since I’ll probably need more than 12 VCCs to get going, and additionally with the paid service for $10/mo, I can become anonymous for some of my transactions if that suits me. Also there is some “Cash Back” which may actually pay for the $10 fee. Not sure.

If you’re in the same situation with your credit card numbers being replaced due to fraud, you may want to check into a Virtual Credit Card service. I suggest creating a separate checking account with your bank first that you can manage online and probably get a Debit Card for that account right away. Maybe you can get the Debit Card via email. We’ll see.

Oh. So the credit card companies are about to lose all of the 2.5% on all my online transactions. Since I’ll be using a VCC service that uses a Debit Card as funding, the VCC service will get the 2.5%. So BofA and Capital One or any other bank will get no cut of any of those transactions. Hummm… You’d think they would be more enthusiastic about supporting VCCs to keep their cut. Oh well. And the VCC service is going to give me 1% back every month too if I’m on the paid plan which will help offset the fee they charge me.

One More Thing

What if credit card numbers were all virtual? What if the plastic only had a bank logo and your name, no number at all. What if the number was either looked up from the last time you used that merchant or created on the fly – maybe with the help of a connection through your phone, when you first used the card at a new merchant. And it had a fall back if you are out of range of internet when you make a purchase; or if you’re phone is out of range of the card or dead at the moment.

These are the kind of things that might bring credit cards into the Twenty First Century. Science Fiction? Right. Hey, it’s just banking. Some banks still use Faxes.

For What It’s Worth,

:ww